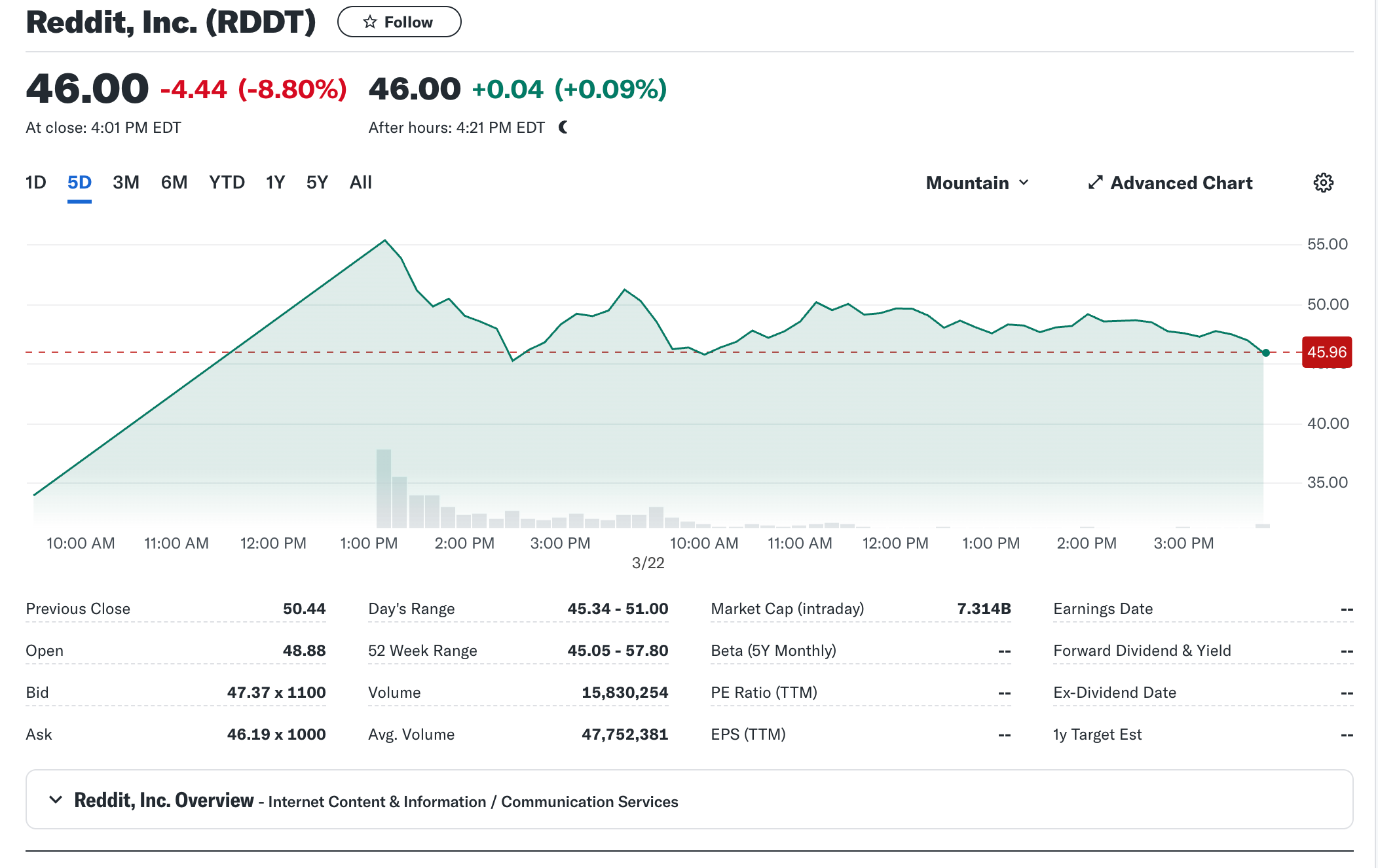

3/22/2024: Reddit IPOed at $34

3/22/2024: Reddit IPOed at $34

closed at $50 yesterday and $46 today

Reddit finally IPOed yesterday at $34 and its stock soared to $54 shortly after it started trading. I got one IPO share and sold it at $54, making a handsome profit of $20. I also owned some pre-IPO shares that will unlock in a few months. I bought these Reddit shares at ~$6/share back in 2014. I believe the post money valuation was $500M when I invested. But there’s a lot of dilution after my investment. The overall valuation grew 15X but my investment only grew ~7.5X and it’s unclear what the RDDT 0.00%↑ stock price will land after the lockup expires.

7.5X is a respectable return. I am very proud to be an early investor and supporter of Reddit. But if you are an LP for a VC that invested in Reddit at the same time I did, after the 2/20 fee structure, I believe your return will be just around 5X, which is actually slightly below QQQ’s 10-year annualized return of 18.14%. Of course Reddit is just an anecdotal example but AFAIK, many of the unicorns that are still waiting for IPOs will end up producing negative returns for investors. The more I understand about VC, the more I believe most investors should just stick with the index funds if investment performance is the main objective. Getting worse returns with no liquidity doesn’t really make a lot of sense. The fees VCs are charging their LPs are too high and VCs have become too competitive to generate alpha even for many top tier firms.