10/19/2023: Tesla Earnings Missed Expectations

Huge revenue growth deceleration

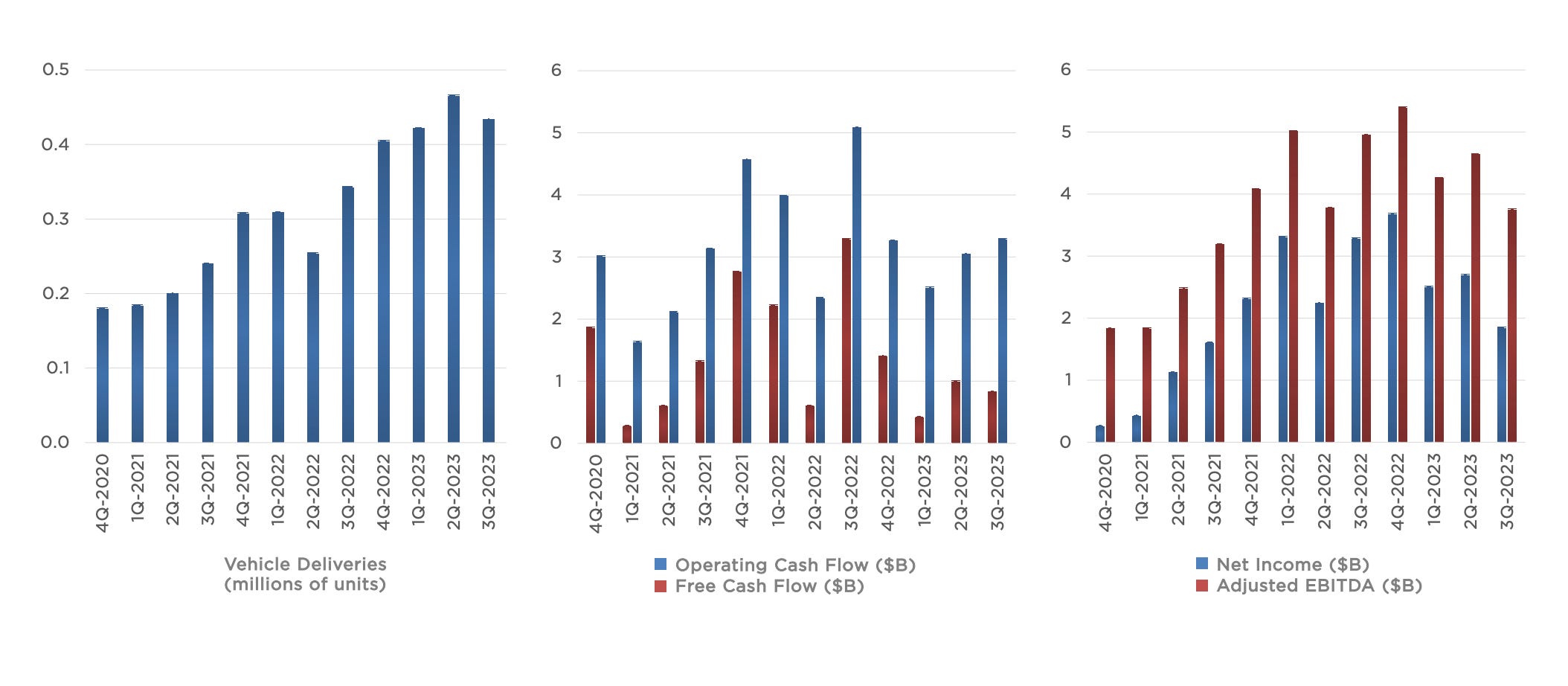

Tesla reported Q3 2023 earnings after market close yesterday. Revenue was $23.35B vs $24.1B expected. EPS was $0.66 vs $0.73 expected. Net income was $1.85 billion, down 44% YoY. Gross margin was 17.9%, down from 25.1% a year ago. Operating margin was 7.6%, down from 17.2% a year ago. Tesla grew revenue 9% YoY in Q3 vs. 47% in Q2 and 44% in Q1. This revenue growth deceleration is staggering. TSLA 0.00%↑ stock tanked 10% in today’s trading session.

Tesla is facing a lot of headwinds right now. The high interest rate environment dampens the demand for cars. Competitors like BYD are gaining ground and might soon outsell Tesla in terms of EV sales. I believe Tesla has good long term prospects though. They are able to sell most of their inventories by cutting prices and still manage to have positive net margins. Beside BYD, Tesla’s competitors are going to get squeezed hard by the pricing war and they might have to exit the market eventually due to staggering losses. Furthermore, Tesla is opening up its EV charging network to other car makers and its energy storage solution Power Wall is gaining ground. I think there will be some short-term pains but Tesla should do well in the long run. I still won’t buy Tesla stock though. It’s still too expensive relative to its business performance.

Tsla is trading at about 250x fcf based on this quarters FCF. More expensive than nvda now with declining revenue and margins as you shared. Vs nvda witb accelerating revenue and margins.

They seem to be cutting /delaying Mexico build. Stock was valued based on management's 50% cagr projections. That seems to be off the table with Mexico delay.

Big reset seems likely.