10/24/2022: Q3 Early Stage Investing Activity Declined Further

Both activity rate and positive activity rate declined

AngelList just published their State of U.S. Early-Stage Venture & Startups Report for Q3 2022. Unsurprisingly, we are seeing QoQ decline in activities and markup rates. Anecdotally, I have observed a general cooling of the early stage funding environment in the past few months. Investors can finally take time to get to know the founders and do proper due diligence before wiring out the money. Unlike last year, many investors were actually taking some time off during summer. In summary, the FOMO environment is over. Pendulum has swung and we are currently in a buyers’ market.

AngelList is the largest early stage funding platform of the world. The report is based on the 9,934 seasoned startup investments on the platform entering into Q3 2022. As you may know, startup investments take a very long time (5-10+ years) to become liquid, a proxy metric people often use to measure the performance of a startup portfolio is the followup funding rate: the percentage of startups that raise additional funding or take an exit after the previous funding has seasoned (typically after 12-18 months).

According to the report, the followup funding rate was 7.4% for Q3 2022 vs. 9.3% for Q2 2022 and 11.6% for Q1 2022, another 20% QoQ decline. Among the startups that received followup funding, 63.4% was positive in Q3 2022, meaning the startup saw its share price increase. The positive rate for Q2 2022 is 77.5% and is 83% for Q1 2022, a 14 percentage points decline QoQ vs 5.3 percentage points decline in the previous quarter.

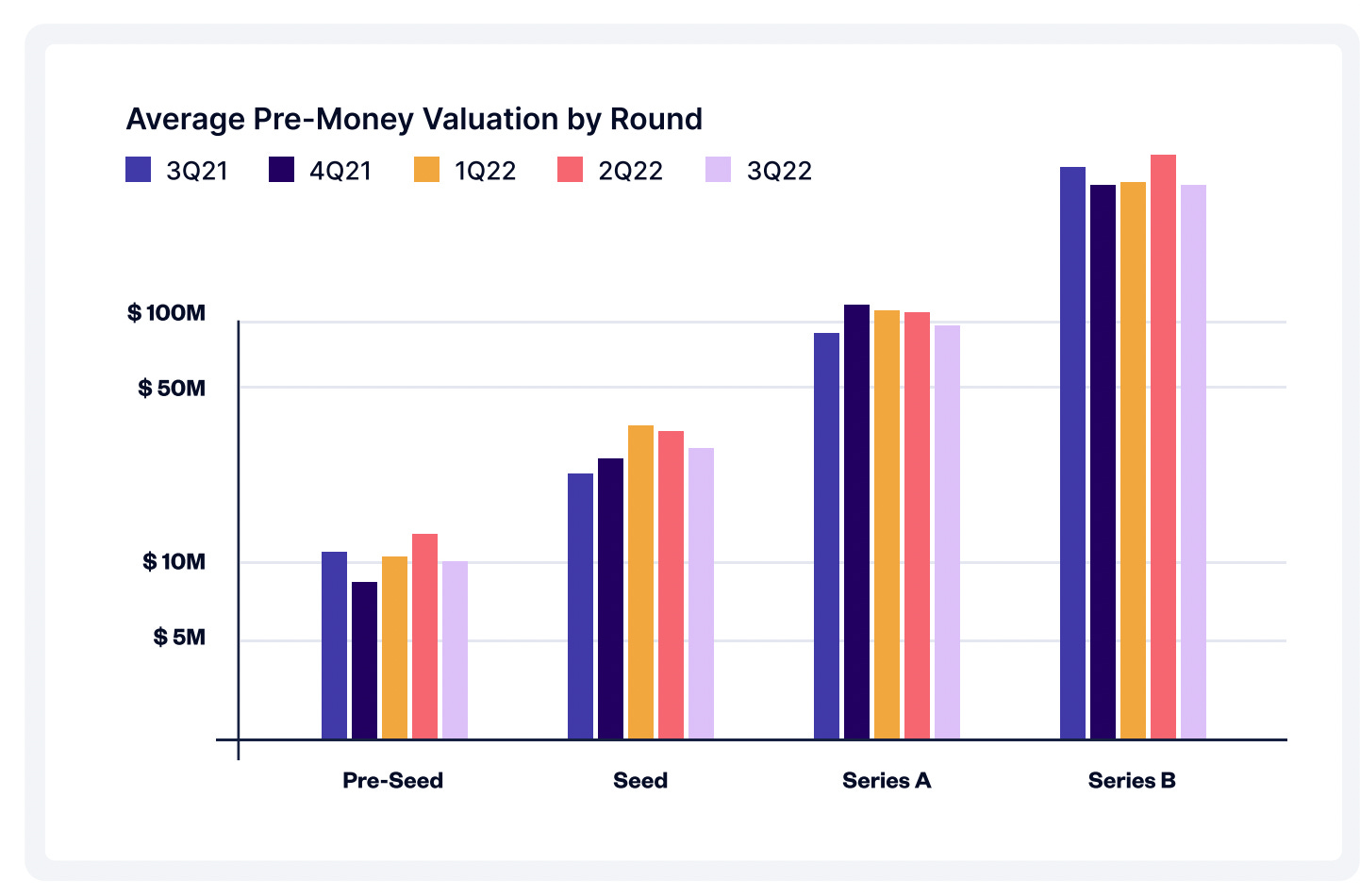

Valuations declined across the board. Pre-seed valuations declined by 19.4% to $10.2M, seed-stage valuations declined by 15.9% to $28M, Series A valuations declined by 13.1% to $86.6M, and Series B valuations declined by 28% to $301M.But compare to Q3 2021, valuations actually rose for seed and series A and only declined marginally for Pre-Seed and Series B. I believe we are not done with the correction on the valuations yet. We are probably going to see more markdowns, shutdowns and recapitalizations next year when startups who raised in 2021 start to run out of money.

2021 increasingly looks more like an anomaly for early stage funding. I do think it’s healthy to go back to the more normal funding environment pre-pandemic where both founders and investors are level-headed. But with the zero-interest rate environment going away, I do worry the appetite for risky investments like angel investing might decrease sharply. I am committed to keeping pace with my investments through this down cycle. I am hopeful that great companies will be built in a tougher environment as constraints and scarcity make people more resourceful and more committed.