3/1/2023: Okta Had a Strong Quarter

Both EPS and Revenue Beat

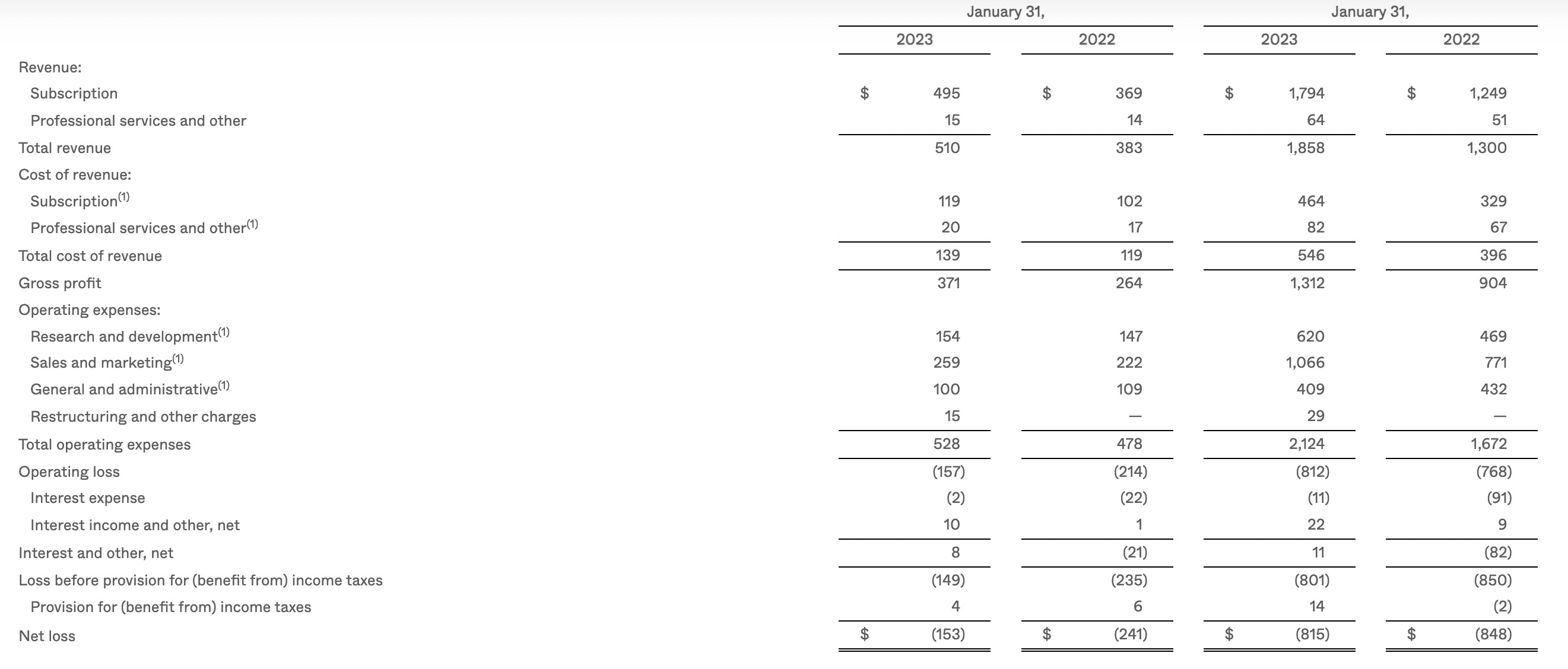

Okta reports quarterly earnings ending 1/31/2023 today after market close. Revenue was $510M vs. $490M expected. Adjusted EPS was $0.3 vs. $0.09 expected. Free cash flow was $72M vs. $5M a year ago. Overall, the numbers are better than expected. Okta is still growing at a healthy clip and they expect revenue for FY 2024 to be between $2.15B to $2.17B or ~17% YoY, which is pretty good considering the current macro environment. After all, their product is essential to enterprises that use cloud software and their only meaningful competition is Microsoft.

OKTA 0.00 stock soared 14% after the report today. Okta’s enterprise value to forward revenue ratio is currently ~5.2, which is well below the historical average of ~8 for SaaS companies. I believe the current tech downturn will bring down the cost for product development and sales significantly for Okta as the inflated tech salaries come down to earth. Let’s give it another 5 years. I believe Okta will be a highly profitable company with a strong moat and their current valuation is very reasonable.