3/24/2023: More Distress Ahead

Someone has to eat the loss

I watched the PBS documentary Age of Easy Money (as shown above) last night. Nothing in the doc surprised me but it was a really good summary of what happened since 2008 and what will be facing in the coming years. The tl;dr is that the US economy and financial system is in big trouble but we can’t keep kicking the can down the road. Now is the time to take the bitter medicine and to hit the reset button. It’s going to create a lot of chaos and wipe out many businesses and individuals. But if we don’t take this opportunity to clean things up, the damage will keep compounding and will eventually explode.

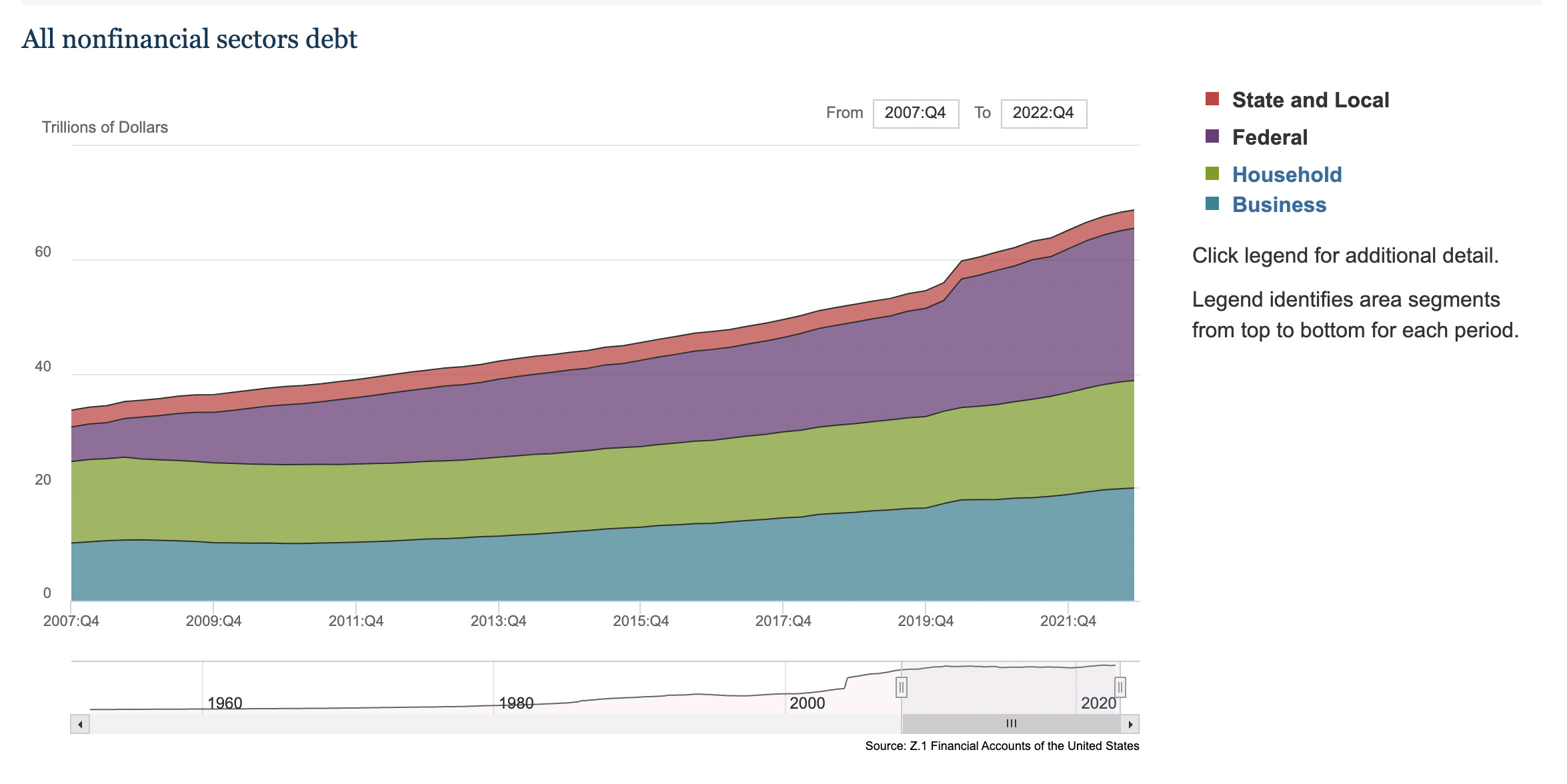

So what exactly does the age of easy money get us into? The zero interest rate policy (ZIRP) made money cheap to borrow and quantitative easing flooded our financial system with money supply. Money became cheap and easy to borrow. But cheap money makes everything else expensive, i.e.: stocks, art, real estate. People borrowed money at low interest rates and loaded up on all kinds of assets. Real assets and securities became unsustainably expensive and businesses and individuals were feeling rich while sitting on a lot of debt. Then inflation hit. The Fed realized their easy money policy was pushing up prices and they needed to start tightening to bring down the inflation. Money becomes expensive and hard to borrow. Asset prices started to deflate but the debt amount didn't shrink. On the contrary, businesses and individuals need to pay higher interest to service their debt. The Fed fund rates went from 0-0.25% to 4.75-5% in the past year. People with variable rate debt are probably scrambling to handle the increased interest expenses.

In addition, valuation of fixed income investments is sensitive to interest rates. If you buy a 10-year treasury note that pays 2% per annum exactly a year ago at $100 and now a newly issued 10-year treasury note pays 3.5% per annum, you can’t sell your treasury note today at $100. You need to offer a discount to compensate for the lower coupon rate. Assuming the 9-year term interest rate is also 3.5%, if you sell your note today, you will only get $88.5 (=PV(1.75%, 18, 1, 100) in Google Sheet). The longer the duration, the deeper the discount is. The 30-year mortgage rate went from 3% to 6% in a year. I just did a calculation in Google sheet. Whoever held the 30-year mortgage debt issued last year is sitting on a ~30% loss right now. According to Bloomberg, 40+% of outstanding mortgages originated in 2020 and 2021. Whoever held those mortgages is ~30% underwater. There’s ~$12 trillion dollars worth of household mortgage debt in the US at the end of 2022. $12T * 40% * 30% ~=$1.4T. In other words, there’s $1+ trillion dollars of unrealized loss on just household mortgages. Someone has to eat that loss as the home owners are not going to pre-pay their mortgages with <3% interest rates. Who is someone? Retail investors, banks, pension funds, college endowments, public institutions and finally the Fed (aka taxpayers) are most likely the bag holders who take the big hit.

All this mess is created by the unsustainable zero interest rate policy. Because of it, we are going to see instability in our financial systems as asset prices collapse and the paper wealth gets destroyed. An even bigger issue here is that this paper wealth didn’t actually do much. A house doesn’t actually increase in actual utility when the price doubles. Same for stocks or a piece of artwork. People felt richer but it was all an illusion. Financial growth is not equal to real economic growth. As the ZIRP era comes to the end, we have a lot to reflect on. Perhaps we should focus on putting money into building things that will generate real wealth for people in the long run such as affordable housing, AGI, semiconductor manufacturing or nuclear power plants, instead of this fake money game driven by the Fed and amplified by over leveraged and over financialized institutions.

gonna be painful next few years for finance... lenders who are locked into low rates / borrowers who are not are going to face some ugly scenarios.