4/12/2023: March CPI was 5.0%

Core CPI 5.6%

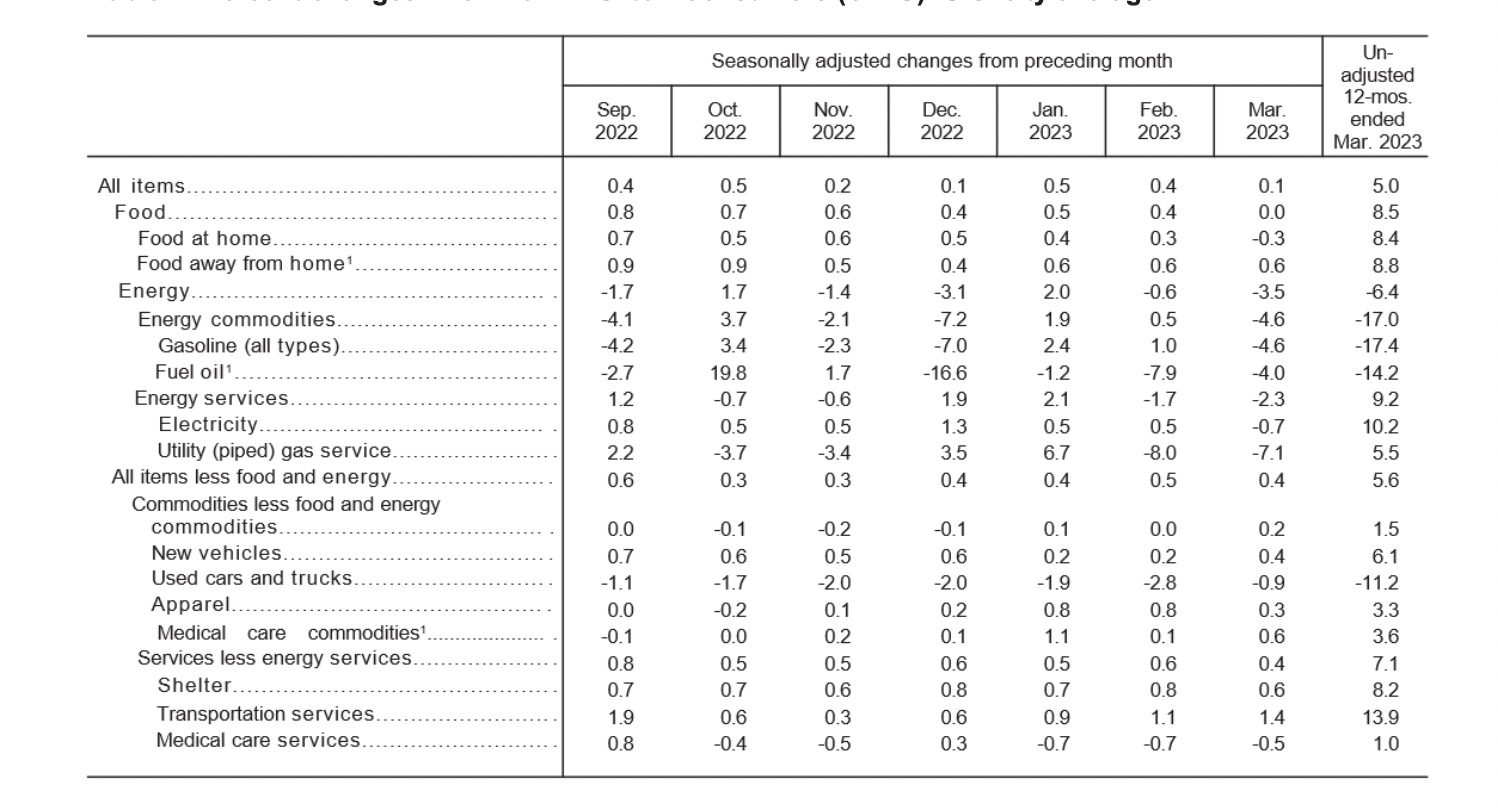

March CPI report is out. Overall CPI MoM rose 0.1% in March vs. 0.4% in February while the core CPI MoM rose 0.4% in March vs. 0.5% in February. Overall CPI YoY rose 5% in March vs. 6.0% in February and 6.4% in January. Core CPI YoY rose 5.6% in March vs. 5.5% in February and 5.6% in January. Overall CPI YoY increase of 5% is the smallest 12- month increase since the period ending May 2021.

Overall, this is a good report. The Food away from home aka grocery prices finally came down. The food prices were kind of out of control. It’s great to see prices seem to stabilize and I can finally have my 3-egg omelette without guilt. Energy prices also trended down 3.5% in March. Core CPI, on the other hand, seems to be quite stubborn and stayed high at 0.4% MoM and 5.6% YoY. I believe the core CPI needs to come down before the Fed will consider cutting interest rates. But according to the report, we are still seeing broad price increases in shelter, motor vehicle insurance, airline fares, household furnishings and operations, and new vehicles. I just got a big sticker shock in summer airfares. It seems like there’s a lot of demand and evil airlines will keep increasing the prices until consumers throw in the towel and stop flying. I bit the bullet and bought the tickets. I am a sucker and there are probably enough people like me that the inflation will stay high for a little while.

People/consumers care about CPI

The fed cares about core CPI, PCE, trimmed mean etc.

What the fed is generally looking to do is remove most volatile (anomalous) numbers from inflation data to determine how broad/sticky it is.

Core CPI moving up is more concerning, than CPI declining is beneficial.

While headline is generally all that matters to markets short term there was also some seasonal adjustment wizardry. Have a look at gas and used car prices non seasoanly adjusted. Compare this to used car wholesale index (which leads consumer 3-4, months) and average gas price data trends.

Wage inflation has cooled some but labour market still too tight to see it get from 5-6% down to 2% with inflation continuing to run at 5%. Workers have the ability in this labour market to demand and get inflation adjusted wage increases.

Add on top of this the new oil spike this month with opec cuts.

March was the bottom for CPI in this downleg.

February was the bottom for core CPI in this downleg.

Markets are forward looking. Liquidity is getting worse as TGA needs 0. Debt ceiling talks are on deck next.