6/15/2023: Probability of Getting Caught

SBF's amoral calculus

(This post was written a week ago as I just landed in Taiwan when this is published.)

Journalist Brady Dale recently published SBF: How the FTX Bankruptcy Unwound Crypto's Very Bad Good Guy. It was a good recap of the FTX fiasco and it went into details on SBF’s thought process. In essence, SBF is using probabilistic thinking to inform his decisions. Moral compass isn’t part of the equation. What matters to SBF is the expected outcome. In his book, it’s all about optimizing for the expected net positive impact. Of course the journalist is not SBF himself so he is paraphrasing what SBF said. It’s entirely possible that SBF is just an impulsive addict with a savior complex. But let’s assume SBF is completely rational and acted based on his philosophical principles. In this framework, one could end up saving the world or going to jail while optimizing for the expected net positive impact.

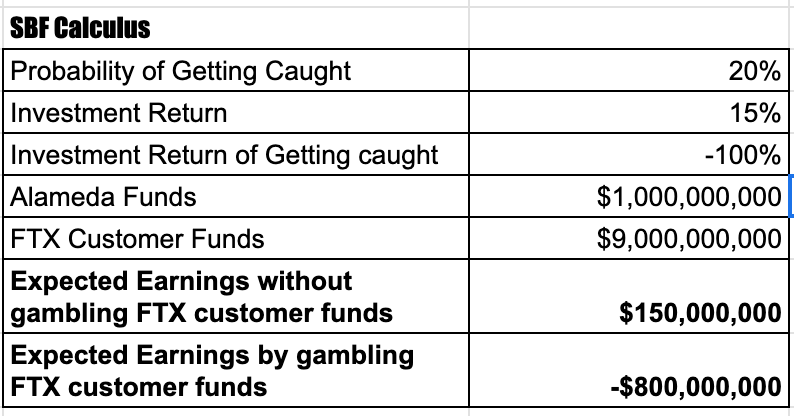

So how does this optimization work? Let me skip some of the technical details and go straight to SBF’s conclusions. Basically, SBF thought if he can make a lot of money, he can give this money to Effective Altruism supported causes to maximize the net positive impact for the world. In order to do that, he tried to make as much money as possible through FTX/Alameda. But in order to make a lot of money, he has to take risks on a large amount of money. If he can take risks on FTX customers’ money in addition to the Alameda money, he can make more money this way and make his impact bigger. But taking risks on FTX customers’ money is illegal, how dare he do that? Well, he thought the probability of him getting caught doing that is very very low and the expected IRR on customer funds is very very high so to him it’s a rational decision to gamble invest customer funds.

Let me illustrate with an example below. Say there’s a 1% chance that SBF gets caught taking risks on customer funds and in that case, the customer withdrawals will end up bankrupting the company, resulting in a 100% loss. But if he doesn't get caught and everything goes according to plan, he will be able to generate a 15% return on the invested amount. Let’s also assume Alameda has $1B of AUM and FTX has $9B of customer funds. With this setup, SBF was deciding if he should gamble on FTX customers’ funds. He calculated the expected earnings based on these two options and concluded that gambling on customer funds is a rational decision as the expected earnings of $1.385B by gambling on FTX customers’ money is way greater by not gambling, which will *only* generate a paltry earning of $150M.

There are many issues with this type of thinking. First, it’s a violation of the contract between FTX customers and FTX exchange. For our society to function well, we expect people to respect the law and contracts agreed upon. The blatant disregard of contract here is astounding. But if we put the ethics aside, the mathematical model used here is highly flawed. The probability of getting caught is by nature very hard if impossible to quantify. SBF *thought* the probability was low but what does *low* mean? It could be 1% or it could be 20%. The expected earnings is $1.385B for the former while -$800M for the latter. In essence, there is a high variability of the expected outcome. In addition, using the expected earnings to make investment decisions is foolish. Expected values are only relevant when you can repeat the decision process for a large number of times. In reality, especially for this particular case, there is no law of large numbers that could be applied. SBF only got to pick his path once. When he decided to gamble on user funds, there are only two binary scenarios where one scenario is catastrophic and the other is positive. Choosing an option that could lead to a catastrophic outcome because the expected earnings is higher while there’s another option available that would lead to a positive outcome with certainty is a bad strategy. Let me illustrate with another example. Say you already have $1B. Here are two options for you to gain more wealth.

Option 1: Make $150M with certainty

Option 2: You could either make $1.5B with 90-99% of probability or lose $1B with 1-10% of probability. When you make that $1.5B, you will have slightly more bragging rights. But when you lose $1B, you will lose reputation and sully your family name for five generations.

Which option will you pick? I will argue only a fool with pick Option 2. The marginal utility is simply not worth it. If SBF were truly intellectually sophisticated, gambling on customer funds would not have been a rational choice.

It’s highly likely that all this supposed *rational* probabilistic thinking is, at the end of the day, a way to rationalize his criminal behavior. SBF was doing all of this to *maximize* his expected positive impact. Positive impact for who? You might ask. For Effective Altruism where you can have a mathematical formula to calculate the number of lives this money made from gambling on customer funds could save. At some point I will write an essay about how fragile EA’s math is but I will save it for another day. Let me just say with EA’s utilitarian framework, almost all fraudulent financial behavior could be rationalized in the name of maximizing impact. I don’t believe SBF was really optimizing for positive impact though. It appears that all the impact talk is just a convenient excuse. He was taking risks on FTX customer funds to maximize his power and status and he thought he could get away with it. (Option 2) And for a while, he did. Oh I forgot to mention the probability of getting caught is increasing over time as the cumulative probability simply accumulates. Chances are there are more SBFs out there in the wild. It’s just that they have not been caught. But they are all the same: SBF, Bernie Madoff, Enron execs, etc. The insane fact is that these people were fabulously rich already before committing frauds but they couldn’t help themselves. Their insatiable appetite for money, power and status ruined lives for their investors, their customers, their families and themselves. It’s stupid and tragic.