7/20/2023: Netflix Q2 Earnings Missed Expectations

$NFLX tanked 8% during the session

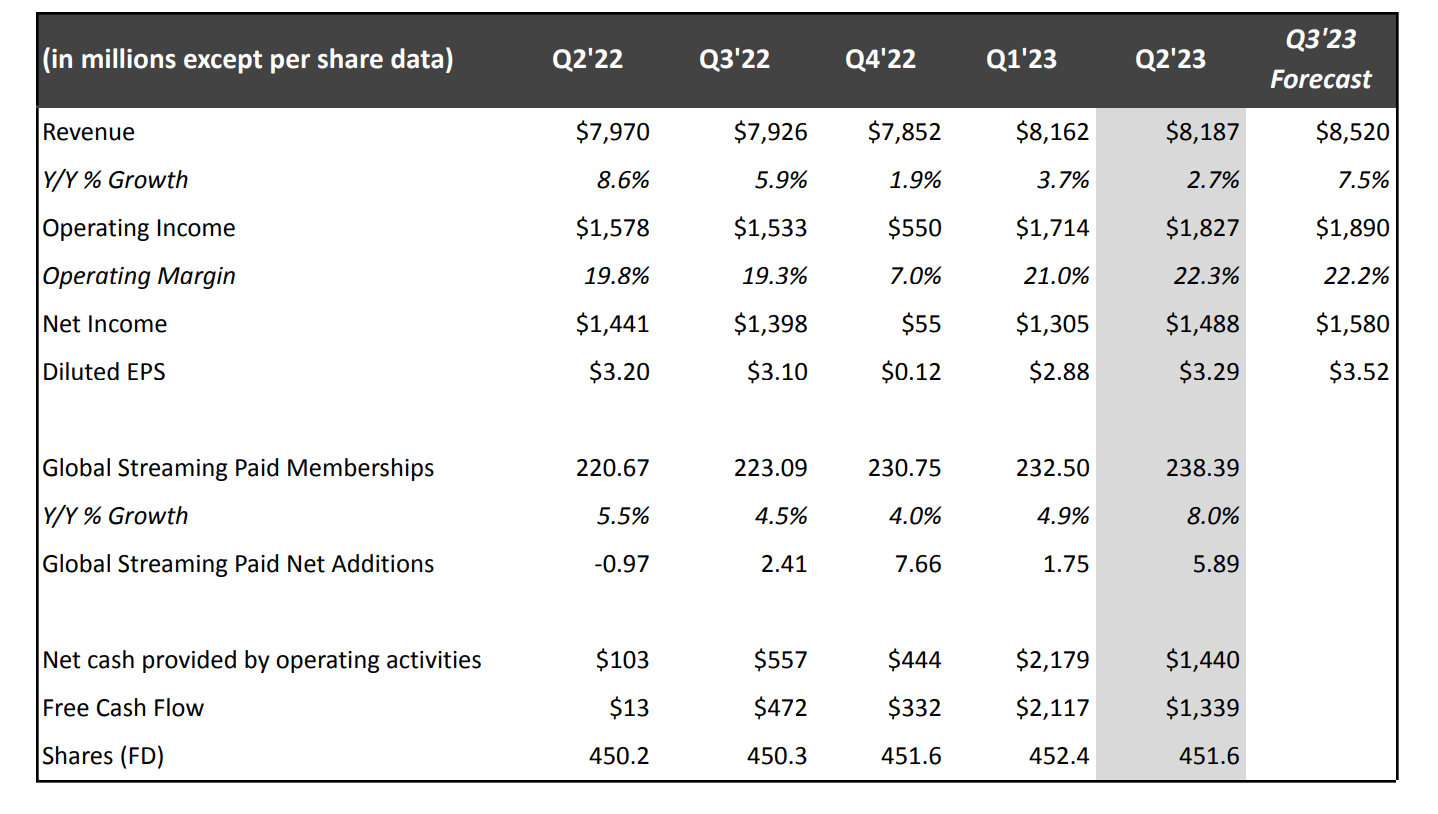

Netflix reports Q2 earnings after market close yesterday. Revenue was $8.19B vs. $8.3B expected. EPS was $3.29 vs. $2.86 expected. 5.9 million subscribers were added in Q2. FCF went from $13M a year ago to $1.339B this past quarter. Netflix increased its FCF forecast to $5 billion for 2023, up from a prior estimate of ~$3.5 billion due to lower spending on content this year. NFLX 0.00 stock has had a huge run up until its earnings yesterday, actually hitting the 52-week high yesterday with 60% YTD return but the Q2 earnings came in light and the stock tanked 8% during today’s trading session.

Reading through the earnings release, it’s mostly about how the company is cracking down on password sharing to improve profitability and revenue growth. I think it’s a good short term strategy but the company gotta reinvent itself and come up with some new growth drivers. Sure, when ad-supported tier and password sharing crackdown come into full effect, their revenue growth can accelerate from the current 2.7% YoY to maybe 15-20%??!! They are currently trading at a very rich valuation of 40X FCF. Does the company really expect password sharing crackdown and ad-supported tier will be enough to maintain the current valuation? I seriously doubt it.