7/22/2022: Confirmed: Early Stage Investing Activity is Tanking

Markup activity is down 25% QoQ

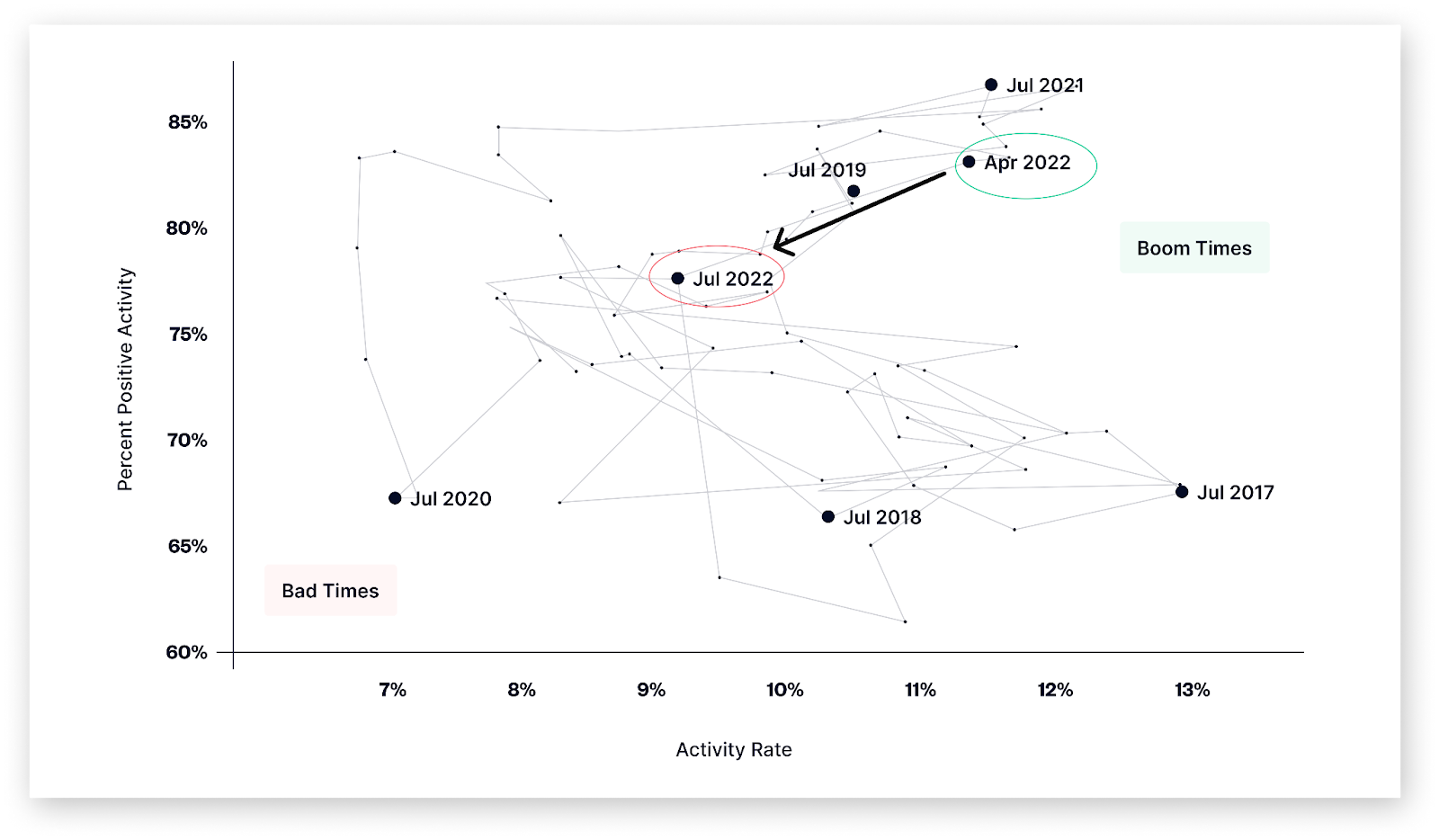

AngelList just published their State of U.S. Early-Stage Venture & Startups Report for Q2 2022 and things are not pretty. They saw the largest quarterly decline in VC performance ever observed in their dataset.

AngelList is the largest early stage funding platform of the world. The report is based on the 8,306 seasoned startup investments on the platform entering into Q2 2022. As you may know, startup investments take a very long time (5-10+ years) to become liquid, a proxy metric people often use to measure the performance of a startup portfolio is the followup funding rate: the percentage of startups that raise additional funding or take an exit after the previous funding has seasoned (typically after 12-18 months).

According to the report, the followup funding rate was 9.3% for Q2 2022 vs. 11.6% for Q1 2022, a 20% decline. Among the startups that received followup funding , 77.5% was positive, meaning the startup saw its share price increase in Q2 2022 vs. 83% in Q1, a 7% decline which marks the second largest quarterly drop in positive activity rate ever (after Q2 2020). In other words, the markup rate, percentage of startups that received followup funding at a higher valuation, is 9.3*0.775 = 7.21% in Q2 2022 vs. 11.6*0.83 = 9.63%, a 25% decline QoQ.

Interestingly, the valuation itself doesn’t move much. Average pre-seed valuations jumped 17% in 2Q22 to $12.6M. Seed-stage valuations declined by a modest 3% to $33.3M, and Series A valuations declined by an even more modest 0.4% to $99.5M. I am a bit shocked that the pre-seed valuation actually went up and the seed/series A valuation remained so high.

If we reference at the previous report in 2021, the median valuation $8M, $15M, $60M for pre-seed, seed, series A respectively in 2021 and $10M, $20M, $70M in Q2 2022. After a super frothy 2021 and a 50+% fall on tech stocks in early 2022, I couldn’t believe we are still seeing a modest increase in startup valuation. The activity rate decline does indicate that investors are getting cautious. We might eventually see a valuation decline but it would probably take another quarter or two for the data to show as it takes time for founders to raise and close a funding round.

I believe we are in a transitory period of startup investments. We are moving back to the more normal time of 2019 where founders need to put in more work for fundraising and investors can do deeper due diligence before making decisions. This is actually a very healthy development. Running a startup is extremely hard and risky. During fundraising, it’s usually a great time for founders to reflect on what they really want from business and life. I am afraid that in 2021, easy money deprived some founders of going through this soul searching process and many founders got into venture-backed startups for the wrong reasons. In tougher times, resourceful founders who can execute would still make it work. But most trendy startups with high burn and a weak business model are probably going to go out of business. This consolidation is healthy and hopefully we will see some great companies built coming out of this market crash.

Awesome data!

When a deal isn't able to get funded where does that appear? We don't have much visibility into this space as you but seems like only top quartile is able to raise?