8/21/2023: Zoom Earnings Beat Expectations

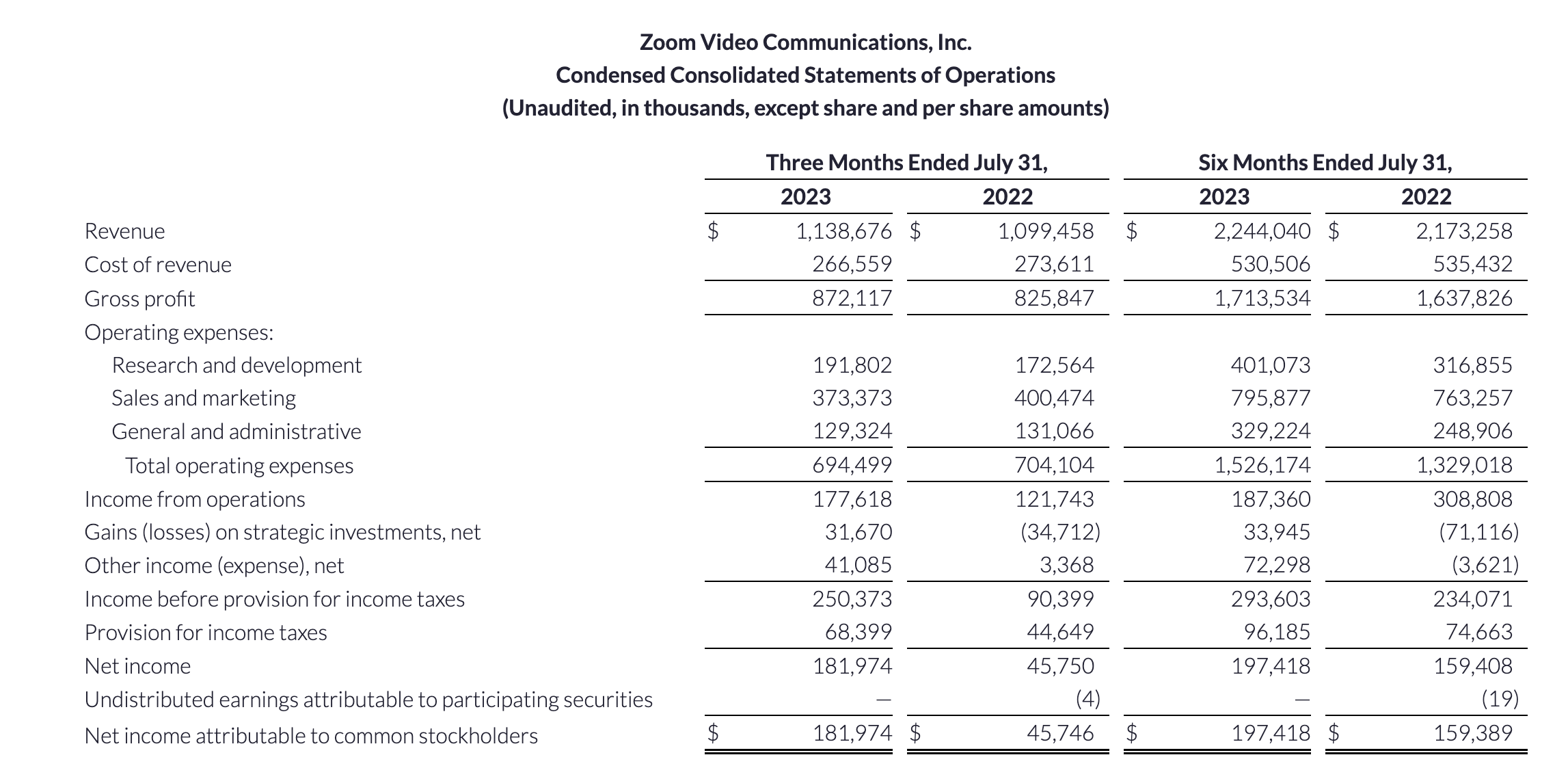

Zoom reported earnings for their second fiscal quarter of 2024 today after market close. Revenue was $1.14B vs. $1.12B expected. Adjusted EPS was $1.34 vs. $1.05 expected. Overall revenue grew 3.6% YoY while enterprise revenue grew 10.2% YoY and the number of enterprise customers with $100K+ contract grew 17.8% YoY.

Overall, it’s a good quarter for Zoom with both revenue and EPS beat. Revenue has stabilized and profit margin has improved. I actually think the company is under monetizing their products. They could probably raise the monthly subscription price for SMB and individual users without much churn. I noticed they already made the free version harder to use if you want a zoom call that’s more than 40 minutes. They won’t let me start a new session immediately after 40 minutes. I have to wait for another 10 minutes to do that. I might eventually cave on that and purchase a subscription as I couldn’t stand Google Meet’s UX. With a $15B enterprise value, $4.6B of annual revenue and ~$1B of annual EBITA,ZM 0.00%↑ stock is very reasonably valued. I am a shareholder and I will continue to hold onto the stock.